Exit Mode · Editorial

The Earnout Trap

How 60% of acquisitions screw founders post-deal, and how to spot it before the LOI is signed. ~12 min read.

I've seen the same scene play out four times.

Founder sells. Headline number is great. £18 million, £24 million, £40 million, doesn't matter, it's a life-changing number on paper. The deal completes. There's a press release. The lawyers shake hands. The founder buys a nice watch.

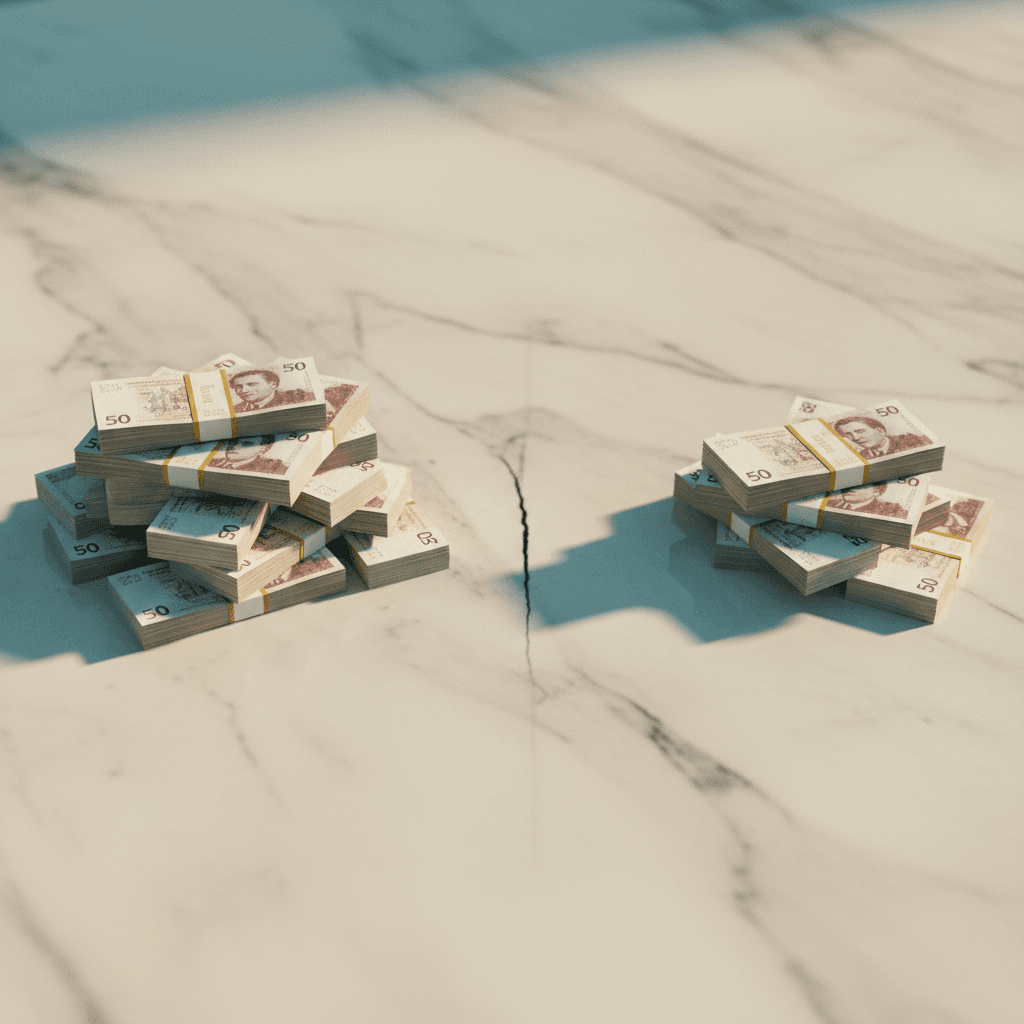

Then comes year one of the earnout. Then year two. By the time the earnout period ends, the cheque the founder actually banked is 50-70% of the headline. In one case, less than 40%.

The numbers vary. The pattern doesn't. Industry data on earnouts is patchy because nobody discloses what they actually paid out, but the most credible private surveys put the share of earnouts that pay in full at well below half. By the time you weight by deal size, founders typically realise something between 50% and 70% of the headline value of an earnout-structured deal.

That's not because most acquirers are crooks. It's because earnouts are structurally rigged in the buyer's favour, and most founders sign them without understanding the games that get played in years one and two of the new structure.

This article is a tour of those games, the clauses that protect against them, and what to do if you're already inside one.

Why earnouts exist

Earnouts exist because buyer and seller disagree on the value of the business, and an earnout is the negotiated bridge.

The founder believes their business will do £6m of EBITDA next year. The buyer believes it might do £4m. They split the difference. Half the consideration is cash at close, and the other half is contingent on the business actually delivering the £6m number, with a sliding scale below that.

On paper, this is reasonable. The founder gets paid for the upside they're promising. The buyer protects against the downside.

In practice, two things happen the day after the deal completes. First, the seller stops controlling the business. Second, the buyer starts running it for their own outcomes, not the founder's. The earnout target sits there in the SPA like a contract neither side is incentivised to honour. The founder is incentivised to maximise the earnout. The buyer is incentivised to minimise it.

The asymmetry is fundamental. Once the founder signs, they have almost no operational control. The buyer has all of it. Every game that follows comes from that asymmetry.

The five games buyers play with earnouts

Game 1: cost allocations. Post-deal, the buyer allocates a share of corporate overhead onto the acquired business. HR, finance, IT, legal, “group services”: a sliver of each gets booked against the earnout entity's P&L. The founder, who used to run with £200k of overhead, now sees £600k allocated. EBITDA evaporates. Earnout target goes from achievable to impossible.

The fix: in the SPA, define the EBITDA basis used for the earnout calculation explicitly. Either it is calculated on a stand-alone basis (no allocations beyond what the business actually had pre-deal) or each allocation must be approved in advance with a justification. Without this, you're paying for the buyer's shared services out of your earnout.

Game 2: ringfenced budgets. The buyer announces a strategic priority and tells the founder to invest in it. Hire a sales team in Germany. Build the new product line. Open the office in Singapore. The founder pushes back: this won't hit the earnout numbers. The buyer says “but it's in the long-term interests of the business.” And they're technically correct.

The fix: agree, in writing, the operating budget for the earnout period at signing. Any deviation from the budget that depresses earnout EBITDA is either added back to the calculation or requires explicit founder consent. This is the single most-skipped negotiation in mid-market earnouts and the single biggest source of leakage.

Game 3: integration drag. The acquired business is asked to integrate with the buyer's tech stack, finance system, brand or ERP. The integration takes 18 months. During those 18 months, no new product features ship, customer renewals stall, and the founder spends 60% of their week in steering committees. The earnout window passes. The targets are missed because the business spent the period being “integrated” instead of operated.

The fix: get the buyer to commit, in the SPA, to an integration timeline that respects the earnout. Specifically: integration milestones cannot occur until after the earnout period ends, OR the earnout target is adjusted downward if integration milestones are accelerated.

Game 4: revenue diversion. The buyer is selling a competing or complementary product line. Post-deal, customers who used to buy from the acquired business are sold the buyer's product instead. The acquired entity's revenue stalls. Earnout misses. Buyer's consolidated revenue is fine.

The fix: include a non-cannibalisation covenant in the SPA. The buyer agrees not to actively divert customers from the acquired entity to other group products during the earnout period, and revenue from cross-sell into the acquired customer base counts toward the earnout calculation, not against it.

Game 5: aggressive accounting. The earnout is calculated on EBITDA. EBITDA is calculated based on accounting policies. Accounting policies are at the discretion of the buyer post-close. New revenue recognition policies, depreciation schedules, capitalisation rules, accruals: any of them can be tightened in ways that depress earnout EBITDA without affecting the buyer's consolidated reporting.

The fix: in the SPA, lock the accounting policies in place for the earnout period. Specifically, the policies in use at the date of completion remain in use for the purposes of earnout calculation. Any change requires founder consent or is added back.

The four contractual protections you must negotiate

Founders rarely lose earnouts because the buyer is dishonest. They lose them because the SPA didn't specify the rules. Four protections, in priority order:

1. EBITDA definition lock. The exact items included and excluded from earnout EBITDA, defined down to the policy level. Cost allocations, accounting policies, one-off items, M&A costs, integration costs: all explicitly carved in or out. Any flex in the definition costs you money post-deal.

2. Operating ringfence. The acquired business operates as a stand-alone entity for the earnout period, with its own P&L, its own hiring decisions, its own budget, and clear rules about what changes require consent. The founder remains accountable for delivering the earnout, but also retains the operational levers to deliver it.

3. Acceleration clause. If the buyer materially changes the strategy of the acquired business, sells it on, lays off the founder before earnout period ends, or otherwise prevents the founder from delivering the targets, the earnout accelerates and is paid out at full or sliding-scale value. This is your insurance against being engineered out of the earnout.

4. Dispute resolution mechanism. A clear, fast, founder-friendly mechanism to resolve disagreements. Independent accountant arbitration with a fixed timetable. Buyer obligation to provide books and records to substantiate calculations. The right to audit. Without this, every dispute becomes a litigation question and litigation is asymmetric: the buyer has more money, more time, and less to lose.

When earnouts are actually fine

Not every earnout is a trap. Three structures are reasonable and work in practice.

The first is a small earnout (10-20% of consideration) tied to a clear, measurable, near-term metric (next-year revenue, contract renewals, specific customer retention). Short window, tight definition, limited scope for buyer interference.

The second is a forward-looking strategic earnout where the founder is genuinely empowered. Founder remains as managing director with budget authority, the earnout targets reflect a plan the founder owned and delivered, and integration is delayed until after the earnout period.

The third is an earnout structured as a roll-up: the founder takes some cash and rolls some equity into the acquirer. The roll equity has the same upside as the buyer's equity, and in many cases is the better path to long-term wealth than betting on a constrained earnout.

What's never fine: a 50%+ earnout, calculated on EBITDA, over three years, with the buyer free to integrate, allocate and reorganise as it sees fit. That's the structure that produces the 40% realisation rates. If a buyer offers it, ask for cash at close at a lower headline number instead. You'll usually be better off.

If you're already inside one

Three things to do if the deal is signed and the earnout is running.

Document everything. If the buyer asks you to make a decision that you believe will affect the earnout, get it in writing. Email the request, email back the implication. The audit trail matters when the dispute comes.

Read the SPA every quarter. Most founders read the SPA once at close and never again. That's a mistake. Re-read the EBITDA definition, the operating covenants and the dispute resolution clause every quarter alongside the actual numbers. You'll spot drift early enough to push back.

Engage your lawyer at the first sign of leakage. By the time the earnout calculation is in dispute, you have weeks not months. Most SPAs have short cure periods on disputes. The lawyers who closed your deal know it best. Use them.

The takeaway

The right way to think about an earnout is not as additional consideration. It is as a hostage. The buyer holds money the founder has earned, and pays it out only if the founder behaves the way the buyer wants for two or three years post-deal. Sometimes that incentive alignment works. More often, the founder discovers that operational control passed at close and the buyer's incentives are not aligned with the earnout.

The single best protection is to negotiate hard on the LOI. The LOI is where the deal's commercial structure gets locked in. By the time you're negotiating SPA wording on cost allocations and EBITDA definitions, you've already lost the argument about whether a 70% earnout is reasonable in the first place.

If you take one thing from this article, take this: every pound of earnout is worth less than half a pound of cash at close, on a risk-adjusted basis. When a buyer offers you a higher headline number with a bigger earnout, run the numbers honestly. The lower cash offer is usually the better deal. The deal you can spend.

Before you sign anything, get the LOI structure right. We have a battle-tested LOI template that flags the eight clauses where founders most often give away value before they realise they're negotiating.

Adam J. Graham